Not all EBITDA improvement stories land the same way. Buyers know the difference before the slide deck loads.

When sellers present value creation work, most buyers apply a discount before the conversation starts. The story sounds familiar because they’ve heard it before, and they’ve seen what happens to those numbers post-close.

Here’s what separates a credible story from a discounted one:

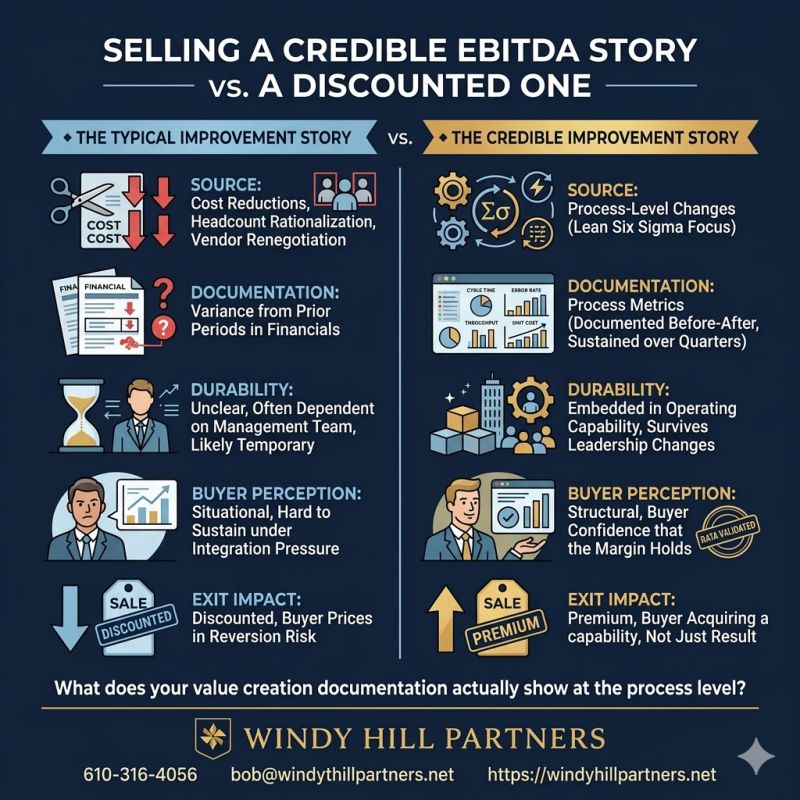

🔹 The typical improvement story

🔸 Source: Cost reductions, headcount rationalization, vendor renegotiation

🔸 Documentation: Variance from prior periods in the financials

🔸 Durability: Unclear, often dependent on the management team that made the cuts

🔸 Buyer perception: Situational, likely to soften under integration pressure 🔸 Exit impact: Discounted. Buyer prices in reversion risk.

🔷 The credible improvement story

✅ Source: Process-level changes with documented before-and-after metrics

✅ Documentation: Cycle time, error rate, throughput, labor cost per unit, sustained over multiple quarters

✅ Durability: Embedded in operating capability, survives leadership changes ✅ Buyer perception: Structural. The margin holds because the process holds. ✅ Exit impact: Premium. Buyer is acquiring a capability, not a result.

The difference is evidence.

A seller who can show process-level documentation, validated with data and sustained without the people who originally drove it, is selling a different asset. LSS creates exactly this kind of record: before-and-after metrics, capability built into the organization, a story a buyer can underwrite.

The multiple premium goes to the seller who can prove the margin is structural.

What does your value creation documentation actually show at the process level?